You can buy the house. But you may not be able to insure it.

In Miami 4 point inspection reports often decide that outcome. It can determine if a home is insurable or too risky for coverage. And it happens more often than most buyers expect.

A bad report can stop a deal in its tracks. No insurance means no mortgage. No mortgage means no closing.

In this guide, you’ll see what can fail, why it fails, and how to avoid delays, surprise repairs, and last-minute deal breakers.

What is a 4 point inspection and why do insurers in Florida depend on it?

A 4 point inspection focuses on four critical systems:

- Roof

- Electrical

- Plumbing

- HVAC (air conditioning)

These are the systems most likely to generate insurance claims. That’s why insurers in Florida require this report, especially for homes over 20 years old.

According to the Florida Department of Financial Services, insurance companies rely on inspections to assess risk exposure before issuing or renewing a policy.

Here’s the key insight:

- A 4 point inspection doesn’t officially “fail”…

- But your insurance can still be denied.

Need a 4 Point Inspection

in Miami-Dade or Broward?

What can fail in a Miami 4 point inspection (and block your insurance)?

1. Roof issues

In Miami, roofs take a beating from sun, humidity, and storms. Therefore, the roof condition is the #1 deal-breaker.

Insurance companies typically look for:

- Age of the roof

- Visible damage or leaks

- Remaining useful life (often at least 5 years)

If the roof looks close to failure, insurers like Citizens Property Insurance Corporation or Universal Property & Casualty Insurance may deny coverage immediately.

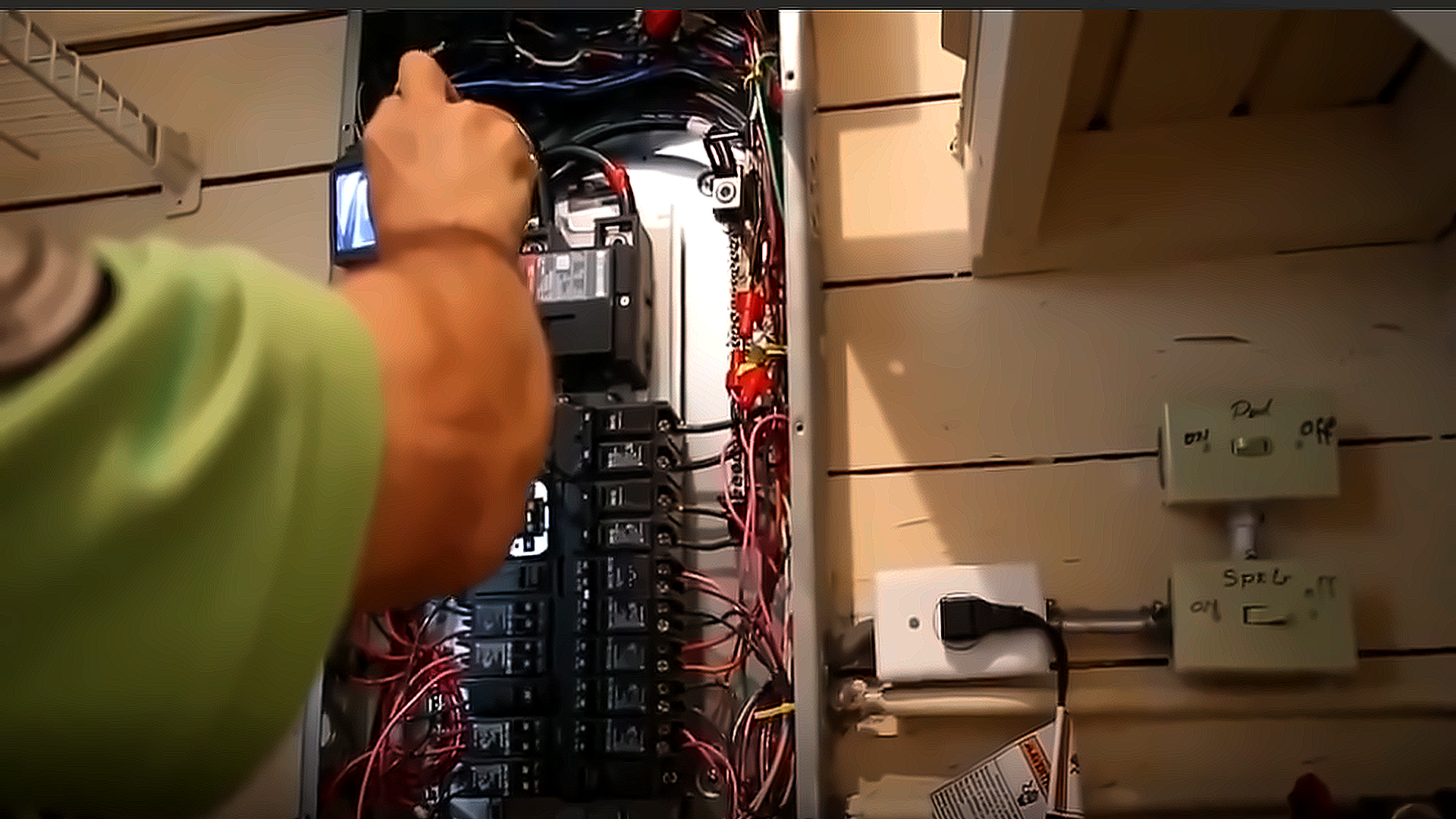

2. Electrical systems that increase fire risk

Outdated panels or wiring can stop your insurance process fast.

Common red flags:

- Old electrical panels (Federal Pacific, Zinsco)

- Aluminum wiring

- Lack of proper grounding

Even if the system works, insurers care about risk, not functionality.

3. Plumbing problems that suggest future claims

Water damage is one of the most expensive insurance issues.

Inspectors look for:

- Old piping materials

- Corrosion or leaks

- Aging water heaters

Small issues today can signal major claims tomorrow.

4. HVAC systems that are too old or unreliable

In South Florida, HVAC is essential.

If the system is:

- Too old

- Poorly maintained

- Not functioning correctly

Insurers may require replacement before approving coverage.

How can a 4 point inspection make or break a deal?

Let’s look at a real scenario in Coral Gables.

- Property price: $720,000

- Built in the 1970s

The buyer ordered a basic 4 point inspection.

Initial result:

- Roof marked as “near end of life”

- Electrical labeled “outdated”

Insurance response:

- Coverage denied

- Closing delayed by 18 days

The deal was at risk.

What changed everything

A second inspection was done with better documentation and tools.

- Drone inspection showed the roof had 6–8 years of life left

- Electrical upgrades were properly documented

- Clear photos aligned with insurer requirements

Final result:

- Insurance approved in 72 hours

- Premium reduced from $5,800 to $3,900 annually

- Deal saved

So, the quality of your inspection report matters

Insurance companies in South Florida are not just reading your report. They are evaluating risk.

- A weak report creates uncertainty—missing details, vague descriptions, or poor photos.

That uncertainty often leads to delays, higher premiums, or even denial.

- A strong report removes that doubt with clear assessments, documented system life, and visual proof.

That difference can mean thousands of dollars.

Insurance cost impact in Renovated Home in Fort Lauderdale

During a home inspection in Fort Lauderdale, a recently renovated property presented a different challenge.

- Purchase price: $540,000

Initial inspection:

- Minor plumbing corrosion

- Aging HVAC

Insurance outcome:

- Conditional approval

- Required repairs within 30 days

- Premium: $4,200/year

After repairs and a proper updated inspection:

- Plumbing fixed

- HVAC serviced

Final result:

- Premium reduced to $3,100/year

- Full coverage approved

How to pass a 4 Point Inspection in Miami

You can’t control the age of a roof or old wiring—but you can control how prepared you are. Here’s what smart buyers and homeowners do:

1. Inspect before the insurance company does

Schedule your own inspection early. This gives you time to fix issues before they become a problem.

2. Document upgrades and repairs

If systems have been replaced or updated, make sure it’s documented. This can make a big difference during underwriting.

3. Work with experienced inspectors

A detailed and clear report helps insurers understand the real condition of the property.

What a Professional Miami 4 Point Inspection Should Include

At Home Inspection Halley, we’ve completed over 15,000 inspections across Miami-Dade and Broward County. The goal is simple. Meet real insurer expectations, not just the minimum checklist.

A proper inspection looks closely at four key systems. But it also goes deeper where it matters.

For the roof, this includes:

- Drone-assisted inspections for a clear, accurate view

- Roof covering type, such as shingle, tile, metal, or flat

- Signs of leaks or water intrusion, including stains, rot, or mold

For the electrical system, inspectors check:

- Type of wiring, such as copper, aluminum, or cloth

- Condition of breakers, outlets, and visible connections

- Proper grounding and bonding

For the HVAC system, the focus is on:

- Signs of damage, leaks, or mold

- Thermostat function and airflow performance

For the plumbing system, the report covers:

- Visible pipe materials, including copper, CPVC, PEX, galvanized steel, or polybutylene

- Water heater age, brand, and safe installation

Beyond the checklist, certification matters. Our inspections are backed by InterNACHI® credentials, including:

- Certified Professional Inspector (CPI)®

- Roof Inspector

- Electrical Inspector

- Mold and Moisture Intrusion Inspector

We also offer bilingual service, including Spanish-speaking inspectors.

With over 21 years of experience, the focus stays the same. Deliver reports that help insurers say yes.

Need a 4 Point Inspection

in Miami-Dade or Broward?

Can you still get insurance if issues are found?

Yes, but it depends on the severity.

In some cases, insurers will:

- Approve coverage with conditions

- Require repairs within a specific timeframe

- Exclude certain risks from the policy

In other cases, they may simply decline the property. That’s why preparation is key.

Miami 4 Point Inspections: What you should not forget

A 4 point inspection is not just a requirement. It’s leverage.

It influences:

- Whether you get insured

- How much you pay

- Whether your deal closes

So before you move forward with a property in Miami, ask yourself:

Is your inspection helping the insurer approve your home… or giving them a reason to reject it?

Because in today’s Florida market, that answer can cost you thousands.

Book Your 4 Point Inspection in Miami Today

If you’ve made it this far, you already understand what most buyers realize too late:

a 4 point inspection can decide whether your deal moves forward—or falls apart.

At Home Inspection Halley, we don’t just check boxes. We deliver clear, detailed reports designed to meet real Florida insurance expectations, so underwriters can make fast, confident decisions.

Whether you’re buying a home or renewing your insurance policy in South Florida, we help you avoid delays, reduce uncertainty, and move forward with confidence.

Schedule your inspection today and make sure your report works for you, not against you.